Empowering Your Financial Future

Our mission is to democratize wealth management by providing access to the sophisticated analytical tools once reserved for the world's top financial institutions.

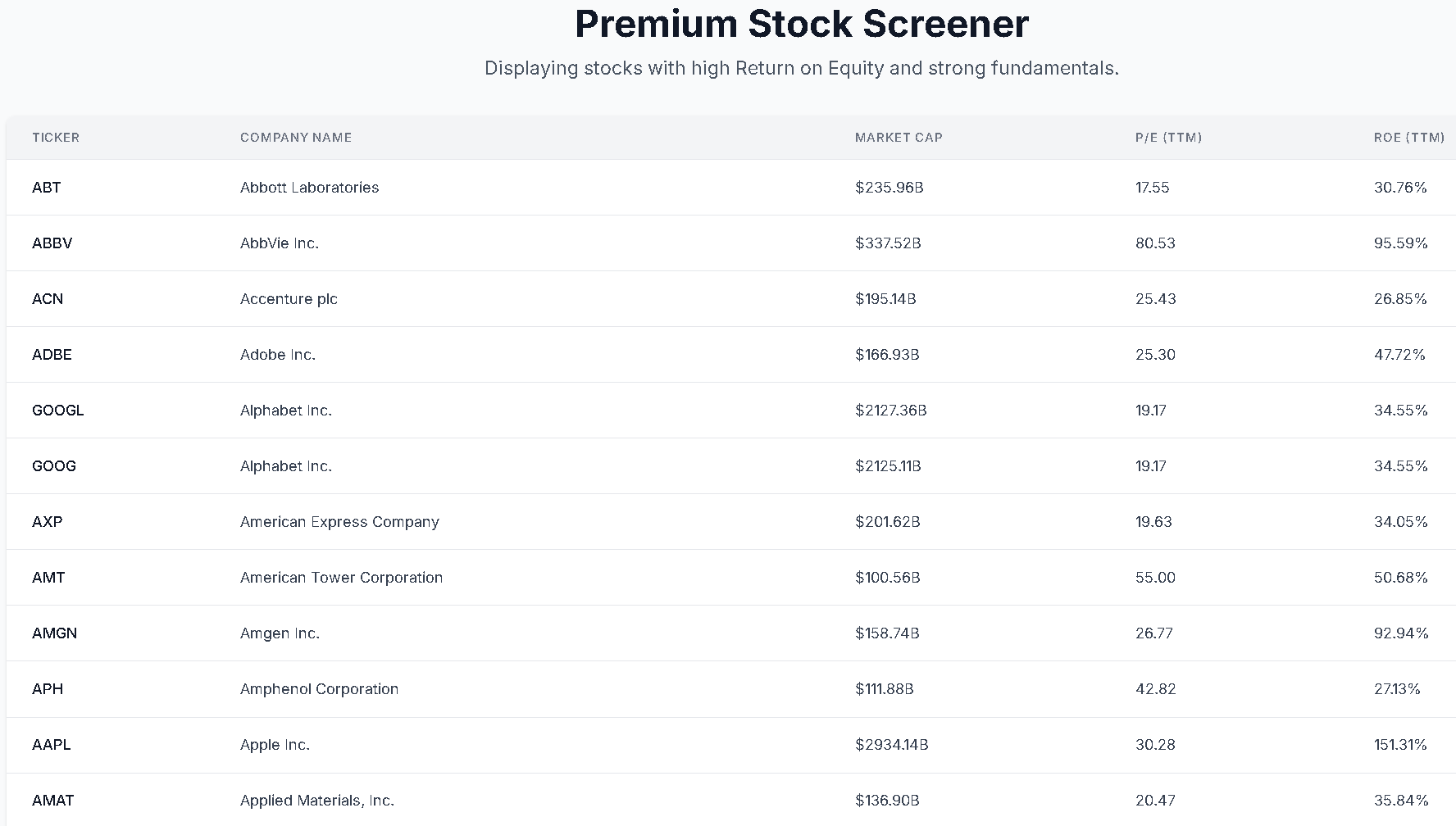

Find Your Next Investment

Our screener allows you to filter through hundreds of stocks in the S&P 500 based on fundamental metrics like profitability (Return on Equity) and valuation (Price-to-Earnings ratio). This is the first step any professional takes: narrowing down a vast universe of stocks to a manageable list of high-quality candidates.

How Quants Use It: Quantitative analysts use screeners to systematically identify companies that match a specific investment thesis, saving thousands of hours of manual research.

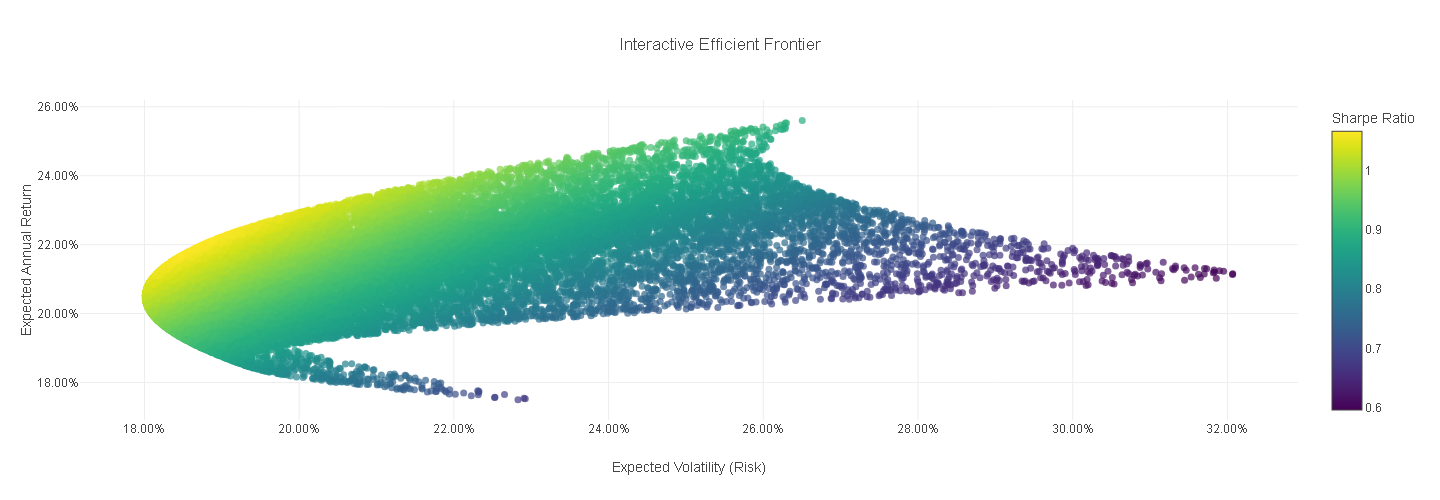

Balance Risk and Reward

Based on Nobel Prize-winning Modern Portfolio Theory, the Efficient Frontier visualizes the optimal trade-off between risk (volatility) and expected return. Our calculator generates thousands of possible portfolios to show you the combinations that offer the highest potential return for a level of risk you are comfortable with.

How Quants Use It: Portfolio managers use this model as a cornerstone of asset allocation to build diversified portfolios that are mathematically optimized for performance.

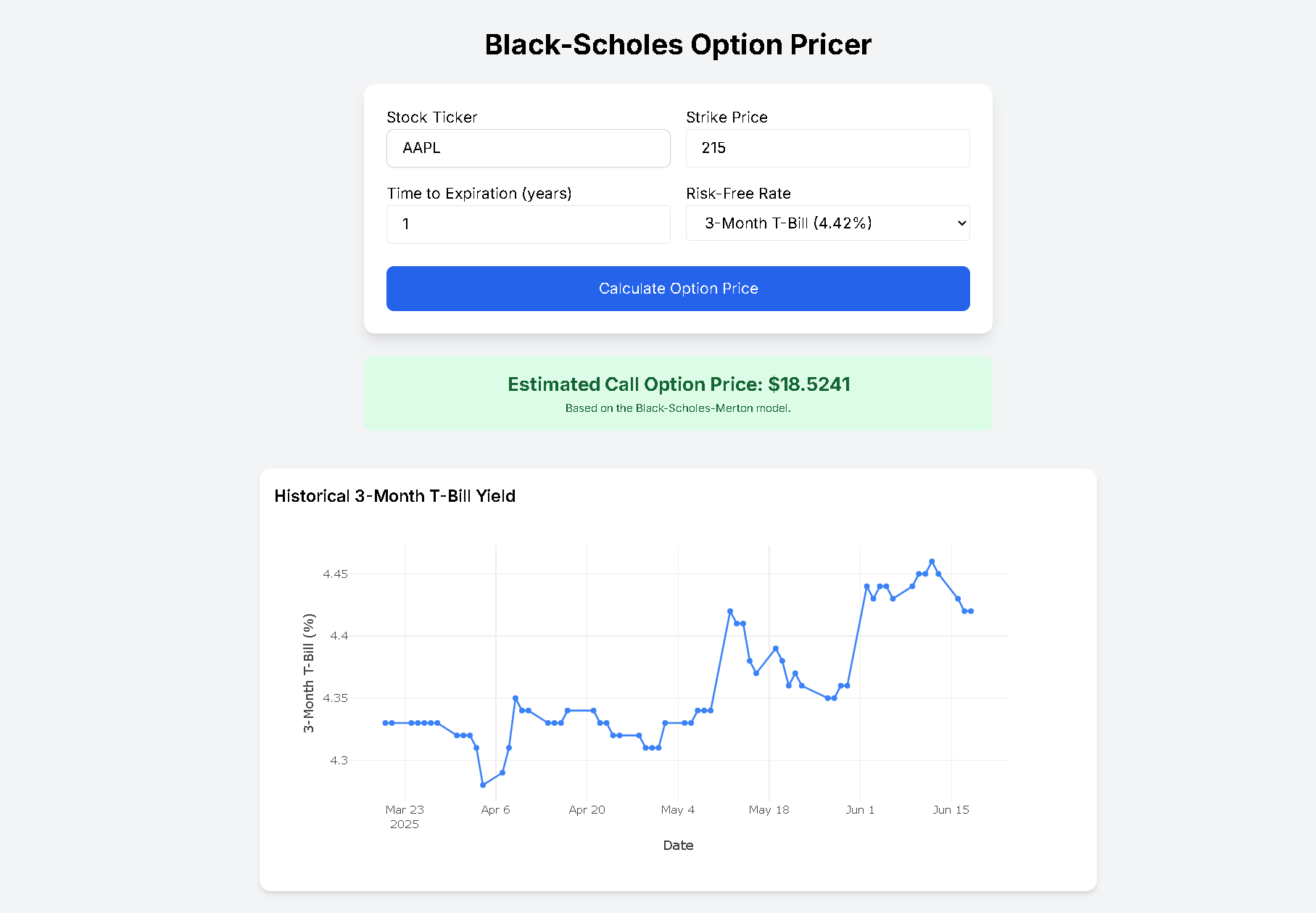

Forecast the Value of Opportunity

The Black-Scholes model is one of the most influential concepts in modern financial theory. It enables precise valuation of stock options by accounting for time, volatility, and risk-free interest rates. This model is not just for Wall Street traders — it's a vital decision-support tool for any investor assessing risk and reward in complex scenarios.

How Quants Use It: Quantitative analysts and options traders use this formula to calculate the fair market value of options, identify mispriced assets, and structure hedging strategies that manage downside risk without limiting upside potential.

What This Means for You: By embedding the Black-Scholes engine into our platform, we give individual investors the power to simulate thousands of market scenarios and make informed decisions with confidence — no PhD required.

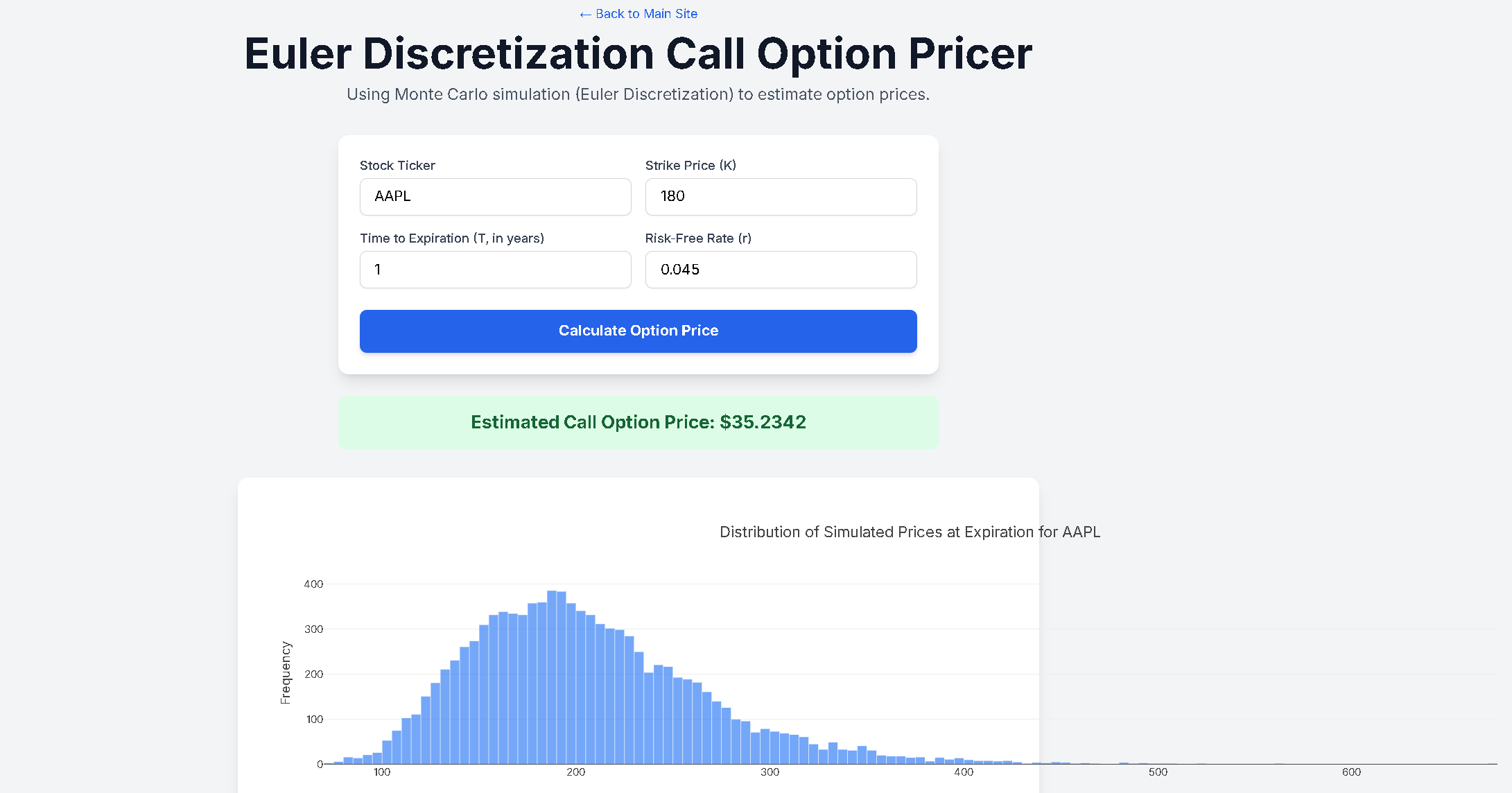

Simulate Market Behavior with Precision

Euler Discretization is a powerful method used in quantitative finance to simulate the future price paths of assets, particularly when modeling stochastic differential equations like those in the Black-Scholes or geometric Brownian motion models. It enables us to approximate how a stock’s price might evolve over time under realistic assumptions.

How Quants Use It: Traders and financial engineers use Euler methods in Monte Carlo simulations to estimate the value of complex derivatives, model option prices under uncertainty, and stress-test portfolios against a wide range of future scenarios.

What This Means for You: With our Euler-powered engine, you can visualize the potential future trajectories of an investment, empowering you to make smarter, more resilient financial decisions. It's like having your own simulation lab — tailored for everyday investors.

See It In Action

Watch this short demo to see how our Forecaster and Efficient Frontier tools can help you make more informed investment decisions.